Natural Gas Forwards Pull Back as Futures Vacillate; Storage Risks Remain

Having entered the summer cooling season at sharply elevated price levels, natural gas forwards pulled back during the May 25-June 1 trading period as the market continued to try to price in risks posed by lagging domestic inventories, according to NGI’s Forward Look.

Fixed price declines of around 25-45 cents for July delivery were the norm throughout the Lower 48 during the period, in line with benchmark Henry Hub, which shed 29.7 cents week/week to fall to $8.396/MMBtu.

In the Midwest, Chicago Citygate fell 35.3 cents to $8.474, while in the Northeast, Transco Zone 6 NY gave back 34.1 cents to end the period at $8.148.

Meanwhile, Nymex futures vacillated during the period, including a 58.2-cent sell-off on Tuesday (May 31), immediately followed by a 55.1-cent rally the next day. The July contract retreated 21.1 cents in Thursday’s session to settle at $8.485 following an Energy Information Administration (EIA) storage print that came in on the higher side of consensus expectations.

[Has Wall Street Created a Legal U.S. Oil & Gas Cartel? If you have been wondering why publicly traded producers in the United States haven’t ramped up supply to meet staggering demand growth, this episode is for you. Listen now. ]

Bearish Storage Miss

The latest EIA report landed on a 90 Bcf injection for the week ended May 27, a figure that exceeded expectations and sent Nymex futures tumbling.

Still, the print provides little cause for comfort, according to Bespoke Weather Services.

It was “understandable” for prices to fall given the miss versus consensus, “but more loosening needs to occur before the market can display any true comfort with the trajectory of storage this summer,” Bespoke said. This would prove especially true should a “hotter pattern unfold once we reach the middle part of this month, which is our expectation as of right now.”

Lower 48 inventories ended at 1,902 Bcf as of May 27, 15.1% behind the five-year average of 2,239 Bcf, according to EIA.

This summer could be the first without a triple-digit build in six years, Energy Aspects observed in a recent research note.

This comes as pricing along the summer strip has been “failing to provide injection incentives,” according to the firm. The market is “seeking industrial price triggers as structural demand growth is hard to reverse.”

Demand for natural gas in the power sector has remained robust despite the higher price levels, and pricing dynamics for coal help explain why, according to RBN Energy LLC analyst Sheetal Nasta.

“A tight coal market and record-high coal prices in the eastern U.S. have suppressed gas-to-coal switching in recent months, despite the gas market also contending with a supply squeeze and gas prices trading at shale era highs,” Nasta said.

Even as natural gas prices have soared, “coal prices have been just as strong,” and this has resulted in “a rather inelastic power demand market for gas like we’ve not seen before,” the analyst said. This means that “as long as the gas market remains tight and coal remains unavailable to pick up incremental power demand, there’s no limit to how high prices for both fuels could go.”

LNG Tilting Toward Asia?

According to NGI’s LNG Insight tracker, volumes flowing to U.S. liquefied natural gas (LNG) export facilities were hovering just under 13 million Dth/d as of Thursday after spending the past week in the 12-13 million Dth/d range.

A “glut” of LNG cargoes into Northwest Europe “has put spot cargo prices in Asia within touching distance of Europe,” according to a recent note from Rystad Energy analyst Lu Ming Pang. “All factors remaining constant — such as no further cuts in Russian gas to Europe — we may see a rebalance of LNG vessels away from the region, which has become a black hole for LNG — drawing in all and every available cargo.”

It’s possible prices in the Pacific could rise high enough to entice LNG cargoes to move there instead of into the Atlantic, where shipping fees are lower, according to the analyst.

“However, if Asia were to pull LNG cargoes into the Pacific due to the impending warmer summer, spot vessels would be deployed on longer routes into Asia Pacific, consuming shipping capacity left on the market, and possibly driving charter rates up higher,” Pang said.

EBW Analytics Group similarly highlighted the potential for demand in Asia to attract more LNG.

“Further, even as European storage inventories refill at a rapid pace, enormous outstanding supply risks from Russian imports could prevent winter risk premiums from sliding too far — even if near-term summer pricing remains subject to more downward pressure,” EBW analyst Eli Rubin told clients.

Given “vastly undersupplied” U.S. storage, “an efficient market should incorporate the risk of converging U.S. and global prices — enabling overseas developments to influence the pricing of Nymex risk premiums, particularly for winter contracts,” Rubin added.

Discounts in Western Canada

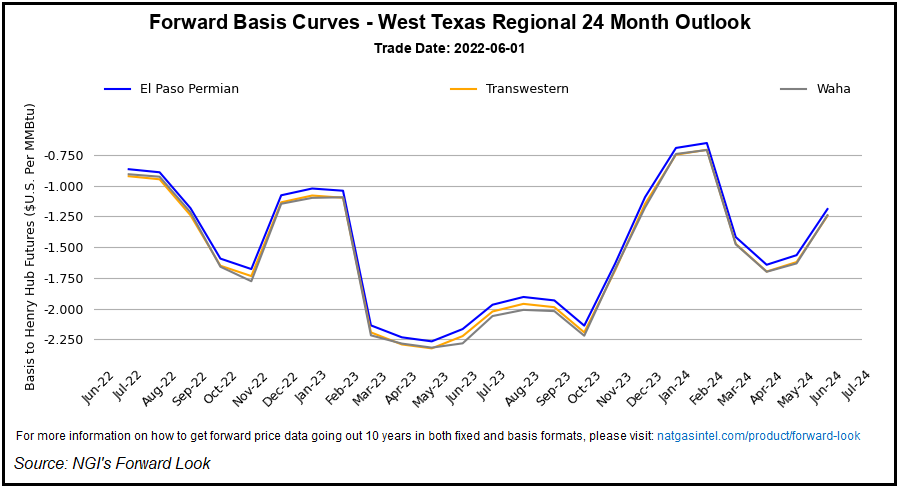

Looking at regional basis shifts for the May 25-June 1 period, there was notable weakening at hubs in the Permian Basin and Western Canadian producing regions.

In the Permian, Waha July basis slid 16.8 cents to end the period at a 90.7-cent discount to Henry Hub, while El Paso Permian fell 16.4 cents to end 86.6 cents back of the national benchmark, Forward Look data showed.

North of the border in Canada, meanwhile, NOVA/AECO C basis tumbled 37.7 cents, ending the period at a $3.024 discount to Henry Hub for July delivery.

Planned maintenance on the Westcoast Energy Inc. system is expected to shut in roughly 280 MMcf/d of flows through an interconnect with the Nova Gas Transmission Line (aka NGTL) system during the month of June, according to Wood Mackenzie analyst Quinn Schulz.

Over the past 30 days, flows through the interconnect averaged 268 MMcf/d and maxed out at around 405 MMcf/d, the analyst said.

Published at Thu, 02 Jun 2022 14:58:01 -0700